Rethinking Money: Crafting a New Economic Paradigm for Global Stability and Equity

Our beliefs regarding money have almost taken on religious fervor, where dissent is not just unwelcome; it’s often ruthlessly punished. It often leads one in a precarious position, as the mainstream options—be it the traditional fiat currency system, assets historically perceived as stable as gold and Bitcoin, or even the concept of debt-free currency championed by Modern Monetary Theory (MMT)—each has inherent critical weaknesses.

To grasp the intricacies, one must consider the unpredictable factors of any financial system: global trade and the concept of credit. Taking a cue from David Graeber’s “Debt: The First 5,000 Years,” it’s clear that credit isn’t a modern invention but rather a foundational element of monetary systems since ancient times.

Taxes are due, and seeds for the next harvest must be bought. Thus, credit in some form—be it primitive tally sticks, bills of sale, purchase orders, or loans—has always been the circulatory system of commerce and governmental income. Credit bifurcates into short-term commercial credit, which is settled upon the delivery of goods or payments, and long-term credit, which is backed by some form of collateral.

In economies where gold and silver are the currency, credit was typically restricted to commercial transactions, as loaning surplus gold and silver was naturally limited by the rarity of these metals. Despite this, the demand for credit persisted and even grew, leading to the rise of small banks in 1820s America. These banks often failed, but they arose to satisfy the growing needs of burgeoning enterprises for expansion credit.

When gold is the sole currency, the extension of credit is naturally capped at a fraction of the gold reserves, a necessary precaution to fulfill customer redemptions and withdrawals, thus constricting credit availability.

Consider our fractional reserve banking system: one ounce of gold in reserve can underpin a loan tenfold its worth—a $2,300 gold reserve could justify the creation of $23,000 in new money since every loan effectively births new money at the moment of its issuance.

The dilemma then emerges with “gold-backed” currency: what occurs when credit inflates the money supply tenfold? The gold reserves end up stretched thinly across a more substantial sum. Consequently, the value of the gold supporting each monetary unit plummets.

In essence, allowing credit to generate money massively waters down the “gold-backed” value of each unit. If credit is constrained to the surplus gold or silver lent at interest, the total credit volume becomes minuscule compared to the total money supply.

The history of Ancient Rome provides a case study in which only gold and silver served as currency. As their Spanish silver mines were exhausted, the influx of new currency ceased, scarcity ensued, and the empire began reducing the silver content in its coinage. Higher-value coins became hoarded treasures, swiftly disappearing from circulation—a practical demonstration of Gresham’s law, where inferior currency displaces the superior.

Rome’s experience also illustrates the influence of trade on currency. The Roman elite, accumulating most of the empire’s “sound money,” indulged in luxuries from afar—silks from China, spices from India, and exotic goods from Africa. This fervent trade siphoned off Rome’s gold and silver wealth to foreign lands in exchange for these opulent imports.

In other words, trade imbalances drain importers of their gold/silver.

Trade imbalances have historically resulted in the outflow of gold and silver from importing nations. As countries import more goods than they export, they must settle this difference by transferring gold and silver to the exporting nations, assuming those are the mediums of exchange.

Over time, this depletion of precious metals can lead to a reduction in the monetary base of the importing country, potentially leading to economic challenges if the country cannot replace the lost wealth or adjust its economy accordingly. This was a common issue under the gold standard, where the fixed relationship between currency and gold reserves could lead to domestic monetary shortages when significant trade imbalances persisted.

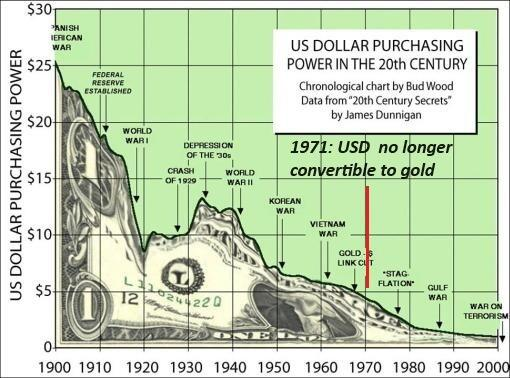

The event known as the “Nixon Shock” on August 15, 1971 (President Nixon’s executive order to suspend the convertibility of the US dollar into gold, effectively ending the Bretton Woods system of international financial exchange) exemplifies the conundrum of trade imbalances for countries on a gold standard. It wasn’t a capricious decision by President Nixon to sever the US dollar’s convertibility to gold; it was an inevitable response to escalating US trade deficits that would have depleted America’s gold reserves. This scenario underscores a classic dilemma: persistent trade deficits ultimately exhaust the ‘sound money’ reserves—gold and silver—halting imports.

Nixon’s decision was also a byproduct of the inherent responsibilities associated with maintaining a global reserve currency. A point often neglected in monetary discussions is the imperative for reserve currencies to circulate globally in sufficient quantities to support international commerce and credit.

Without an ample supply of the reserve currency, scarcity impedes its global utility. As the world economy expanded, so did the demand for US dollars, necessitating ongoing trade deficits to infuse the dollar across international markets.

The argument that relinquishing the dollar’s reserve status might be beneficial ignores the perspective of exporting nations, which rely on the consistent inflow of dollars. Also overlooked is the inescapable nature of trade deficits for nations reliant on imports for essential resources like food and energy.

A world economy constricted by limited credit and trade would starkly contrast with today’s environment. Such an economy might be sustainable with less consumption, but it’s uncertain if this would foster welcomed changes or enhance stability. The aim should be to evolve towards a global economic system that facilitates equitable prosperity without impoverishing the majority.

It’s also worth noting that gold convertibility did not safeguard against inflationary pressures, as evidenced by the dollar’s declining purchasing power during the 20th century, even when it was pegged to gold.

The flood of precious metals from the Americas in the 16th and 17th centuries precipitated a devaluation of gold and silver in Europe, further demonstrating that global market forces ultimately dictated values, including those of currencies, commodities, and labor. Any attempts by states to artificially fix prices only lead to the emergence of black markets.

The inception of fiat currencies was an escape from the constraints posed by ‘sound money’ limits on credit and trade. Yet, the well-documented pitfalls of fiat currencies include the perennial risk of overexpansion. According to Modern Monetary Theory (MMT), or the concept of debt-free currency, excessive currency issuance without corresponding economic growth precipitates hyperinflation.

Borrowing funds into existence by issuing government bonds might mitigate outright currency devaluation but introduces interest expenses—disproportionately benefiting the wealthy, who hold the majority of financial assets—and can suffocate economic dynamism, leading to periods of stagflation or decline.

Hence, we are challenged to envision alternatives to our present system, as it seems bereft of viable solutions. Debt-free money risks hyperinflation, ‘sound money’ tends to accumulate with the affluent, and debt-fueled currency can lead to economic stagnation. The task is to conceptualize a novel economic framework that avoids these pitfalls.

Given these stark realities, it becomes clear that we must pioneer a new economic paradigm—one that transcends the limitations and systemic flaws of our current framework. The pursuit of a viable alternative demands creativity and a willingness to reassess fundamental economic principles.

As we advance, we must forge a system that harmonizes currency issuance with genuine productivity, distributes wealth more equitably, and decouples the vital mechanisms of credit and trade from the cyclical perils of boom-and-bust dynamics. This is not merely an academic exercise but an urgent imperative to prevent the erosion of economic vitality and safeguard a stable and prosperous future for the global community. The future of our economy hinges on our ability to conceptualize and implement an innovative approach that effectively addresses these multifaceted challenges.

Responses